On 1 June 2026, the State Council of the People’s Republic of China (the “PRC”) published the Regulations on Outbound Investment (State Council Order No. 837) (《国务院关于对外投资的规定》(国令第837号)) (the “2026 Regulations”)1 effective from 1 July 2026. The 2026 Regulations are the first PRC State Council-level administrative regulations to comprehensively govern outbound investment, sitting above and operating alongside the existing departmental rules of MOFCOM, the NDRC and SAFE that have framed Chinese outbound direct investment (“ODI”) for more than a decade.

The 2026 Regulations are more than an administrative consolidation. Enacted under the PRC Foreign Relations Law (《中华人民共和国对外关系法》) and the PRC Foreign Trade Law (《中华人民共和国对外贸易法》), they reflect a marked shift towards a more security-driven and coordinated approach to outbound capital under which (i) export controls are embedded directly into outbound investment activity; (ii) a strengthened national security review applies across the full life of an investment, including exits; and (iii) the PRC State Council is given an express statutory platform to investigate foreign investment barriers and to adopt countermeasures against foreign states, organisations and individuals that discriminate against Chinese investors. The framework is supported by robust enforcement tools, including orders to unwind investments, monetary penalties and multi-year bans on outbound investment activity.

This Newsletter reviews the PRC outbound investment legal landscape, analyses the key provisions of the 2026 Regulations from the twin perspectives of (i) the supervisory powers of the PRC authorities and (ii) the obligations of investors making outbound investments from within the territory of China2. It is important to note that both domestic Chinese entities and foreign invested entities established in China are treated as “Chinese investors” under the 2026 Regulations. This Newsletter also assesses the geopolitical and practical implications for international businesses, joint venture partners and financiers transacting with Chinese counterparties.

China’s 2026 Regulations Key Features

- A unified, security-anchored framework. The 2026 Regulations establish full life-cycle supervision of outbound investment by Chinese investors, including Chinese enterprises, other organisations and, for the first time at this level, resident individuals, expressly anchored in the PRC’s holistic approach to national security and the coordination of development and national security (Article 33).

- Export controls embedded in outbound investment. Chinese investors must not export or use goods, technologies, services or related data subject to PRC export prohibitions in connection with outbound investment, and require authorisation for restricted items, the application of which extends to cross-border secondment of technical personnel, technical guidance and training (Article 13).

- National security review across the investment life-cycle. A strengthened outbound investment security review applies to investments as well as to subsequent transfers and disposals of related assets, rights and equity which affect or may affect national security, with mandatory duties of cooperation (Article 15).

- Investigation and countermeasure powers. MOFCOM may investigate foreign investment barriers, and the PRC State Council may adopt countermeasures, including counter-sanction listings, trade and investment restrictions and entry bans, against foreign states, organisations and individuals whose measures harm Chinese investors (Articles 23–25).

- Enforcement with real teeth. Sanctions include orders to cease and unwind investments, confiscation of unlawful gains, fines of up to 10‰ of the investment amount, personal fines on responsible officers and bans on outbound investment activity of one to three years (Articles 27–29).

- A coordinated legal architecture. The 2026 Regulations should be read alongside State Council Order No. 835 on Provisions of Anti-undue Extraterritorial Jurisdiction (April 2026). Together they signal that compliance with foreign regulatory requirements may itself become a source of legal risk in China, sharpening conflict-of-laws exposure for multinational groups.

PRC Outbound Investment Regulatory Framework: the NDRC, MOFCOM and SAFE Rules

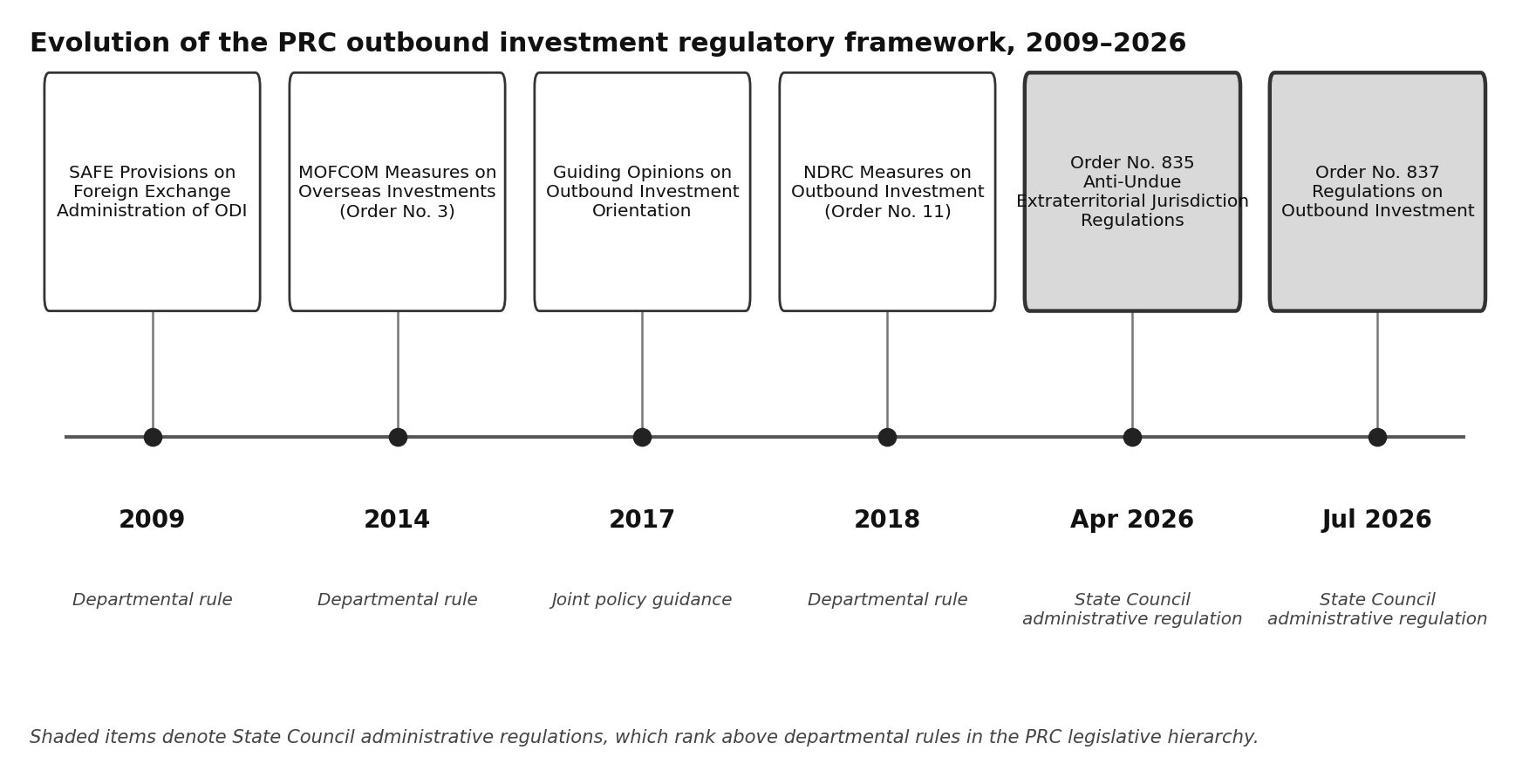

For more than a decade, outbound investment from Mainland China has been administered principally by three PRC authorities: the Ministry of Commerce (“MOFCOM”), the National Development and Reform Commission (“NDRC”) and the State Administration of Foreign Exchange (“SAFE”). The principal rules have been departmental measures/provisions:

- the Administrative Measures on Overseas Investments (《境外投资管理办法》), issued by MOFCOM and effective from 6 October 2014 (the “MOFCOM Measures”);

- the Administrative Measures for the Outbound Investment of Enterprises (《企业境外投资管理办法》), issued by the NDRC and effective from 1 March 2018 (the “NDRC Measures”), supplemented by Q&As published on the NDRC’s website from time to time; and

- the Provisions on Foreign Exchange Administration of the Overseas Direct Investment of Domestic Institutions (《境内机构境外直接投资外汇管理规定》), issued by SAFE and effective from 1 August 2009, together with subsequent SAFE rules and circulars.

As administrative regulations promulgated by the PRC State Council, the 2026 Regulations rank above these departmental rules in the PRC legislative hierarchy and will prevail in the event of inconsistency once in force. Significantly, the 2026 Regulations do not repeal the MOFCOM Measures, the NDRC Measures or the SAFE rules: the existing approval, filing and foreign exchange registration machinery continues to apply, now under an overarching State Council framework. It is possible MOFCOM, the NDRC and SAFE may revise or supplement their departmental rules in due course to align with the 2026 Regulations.

Figure 1: Evolution of the PRC outbound investment regulatory framework, 2009–2026

Application to Hong Kong, Macau and Taiwan Investment

Of particular relevance to Hong Kong: Article 32 provides that the administration of investment by Chinese investors into the Hong Kong Special Administrative Region, the Macau Special Administrative Region and Taiwan is to be conducted by reference to the 2026 Regulations as outbound investment. This regulatory position is consistent with the MOFCOM Measures and the NDRC Measures. Hong Kong remains the leading conduit for Mainland ODI, and structures routed through Hong Kong holding companies should be reviewed in the context including the security review and export control provisions discussed below rather than assumed to fall outside it.

Scope of the 2026 Regulations: Definitions of Investment and Investor

Article 2 applies the 2026 Regulations to outbound investment by investors within the territory of China. “Outbound investment” under the 2026 Regulations is defined broadly as activities by which investors, directly or indirectly, acquire ownership, control, operational and management rights or other related rights and interests in enterprises, assets or otherwise in other countries or regions, whether by contributing assets or equity or by providing financing or guarantees. The express capture of indirect acquisitions and of financing and guarantee structures is consistent with the NDRC Measures and confirms that offshore-intermediated structures fall within the regime.

Outbound Investment by PRC Resident Individuals

In practice, Chinese individuals have generally been unable to make direct outbound investments,4 because the MOFCOM Measures and the NDRC Measures define “outbound investment” by reference to investment by an enterprise located within China.5 Article 2 of the 2026 Regulations breaks new ground: “investors” expressly include enterprises, other organisations and resident individuals within China (which include foreign invested entities established in China). Article 33 provides that specific administrative measures for outbound investment by resident individuals will be formulated by the investment and commerce departments of the State Council. Detailed implementing rules opening (and regulating) direct outbound investment channels for PRC individuals are therefore likely to follow – a development of obvious significance for private wealth, family office and fund structuring through Hong Kong.

Investment in Overseas Financial Markets and Re-investment of Proceeds

Article 33 also expressly extends the framework to investment by Chinese investors in financial markets outside China (whether using their own funds, funds raised from third parties or entrusted funds) and to the re-investment outside China of assets, rights and interests derived from outbound investments. Portfolio investment and the redeployment of offshore proceeds are thereby brought within the same overarching regulatory perimeter as real-economy ODI, closing a perceived gap in the existing departmental rules.

Encouraged, Restricted and Prohibited Outbound Investments under PRC Law

Article 11 provides that the investment and commerce departments of the State Council, together with other relevant departments, will formulate, adjust and implement outbound investment policies, during which they will specify encouraged, restricted and prohibited categories of outbound investment by reference to national economic and social development needs and the investment environment and risk profile of host countries and regions.

The existing three-tier classification is retained. It originates in the Guiding Opinions on Further Guiding and Regulating Outbound Investment Orientation (《关于进一步引导和规范境外投资方向的指导意见》) jointly issued in August 2017 by the NDRC, MOFCOM, the People’s Bank of China and the Ministry of Foreign Affairs, which remain effective. In outline:

- Encouraged investments include Belt and Road infrastructure and connectivity projects; investments exporting quality production capacity, equipment and technical standards; cooperation with high-technology and advanced manufacturing enterprises and offshore R&D centres; prudent participation in oil, gas and mineral resources exploration and development; agricultural cooperation; and services sectors such as commerce, culture and logistics, including the establishment of offshore branches by qualified financial institutions.

- Restricted investments include those in sensitive countries and regions (no diplomatic relations, in conflict, or restricted under treaties to which China is party); real estate, hotels, cinemas, entertainment and sports clubs; offshore equity investment funds or platforms without specific underlying industrial projects; investments using outdated equipment failing host-country technical standards; and investments failing host-country environmental, energy consumption or safety standards.6

- Prohibited investments include those involving the unauthorised export of core military technologies and products; the use of technologies, processes or products whose export from China is prohibited; gambling and pornography; investments prohibited under international treaties to which China is party; and investments that endanger or may endanger China’s national interests or national security.

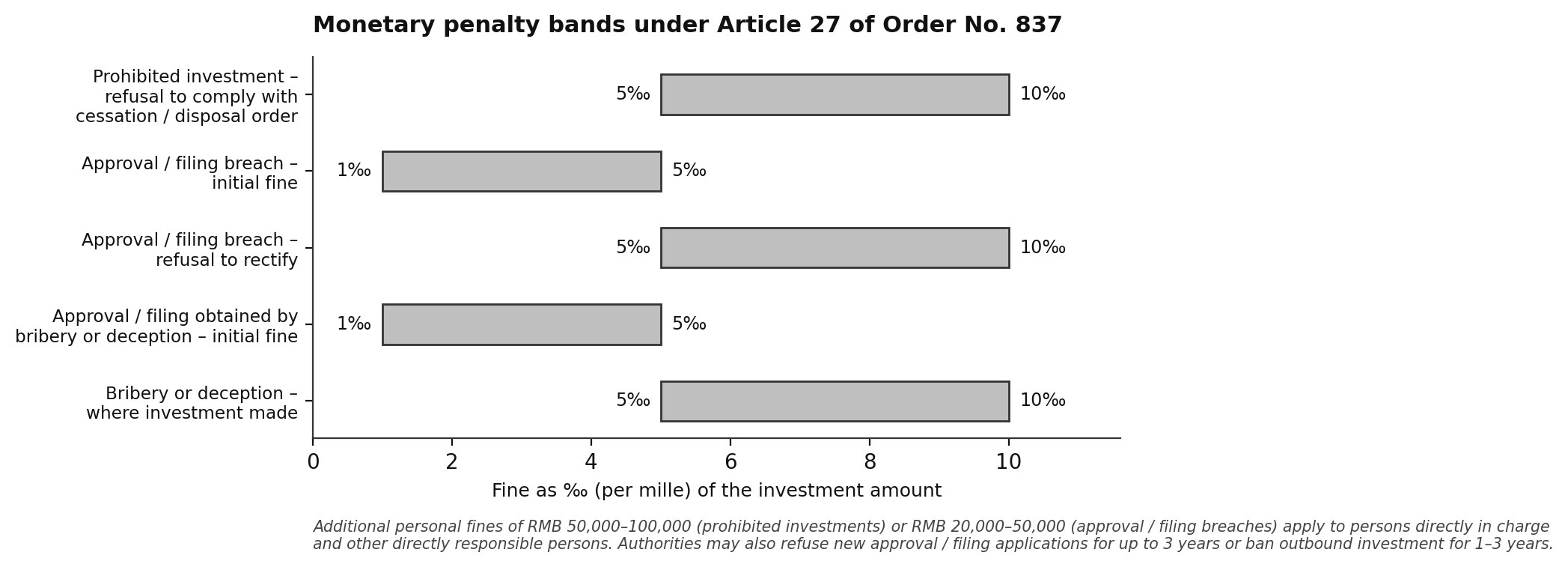

Where a Chinese investor makes a prohibited investment, the PRC authorities may order cessation of the investment, disposal of shares and assets within a prescribed period and confiscation of unlawful gains. Refusal to comply may lead to fines of 5‰ to 10‰ of the investment amount, with personal fines of RMB 50,000 to RMB 100,000 on persons directly in charge and other directly responsible persons (Article 27, paragraph 1).

National Security Review of China Outbound Investment (Article 15)

Article 15 directs the Chinese government to improve the outbound investment security review system: the investment and commerce departments of the PRC State Council, with other relevant departments, will conduct security reviews of outbound investments, as well as transfers and disposals of related assets, rights and equity, that affect or may affect China’s national security. Organisations and individuals must assist and cooperate, may not refuse or obstruct review, and must comply with review decisions.

National security analysis is already built into the NDRC Measures: an application for approval of a sensitive project must analyse the project’s impact on China’s national interests and national security, and approval from the NDRC is conditional on the absence of threat or damage to them. The 2026 Regulations go materially further in two respects. First, review is framed as a standing system applicable to any outbound investment affecting or potentially affecting national security, not merely as an element of sensitive-project approval. Secondly, review expressly extends beyond the initial investment to subsequent transfers and disposals so that the sale or restructuring of an offshore subsidiary, or a transfer of control over an offshore asset originally acquired as a PRC outbound investment, may itself attract security review. Exit planning, secondary sales and intra-group reorganisations involving Chinese-invested offshore vehicles should be diligenced accordingly.

Where Chinese investors refuse to cooperate with security review under the 2026 Regulations, submit false materials or conceal information, or fail to comply with review decisions, the PRC authorities may order rectification, confiscate unlawful gains and impose fines. Where national security is endangered, the PRC authorities may order measures to eliminate the impact, ban the investor from outbound investment for one to three years and, where the investment has been made, order its cessation and the disposal of shares and assets within a prescribed period (Article 28).

Convergence with Foreign Outbound Investment Screening Regimes

Article 15 is broadly comparable in structure to the United States’ outbound investment security programme established by Executive Order 14105 (commonly known as “Reverse CIFUS”) and implemented by US Treasury regulations in effect since January 2025, and to the outbound screening mechanisms under consideration in the European Union and elsewhere. Each regime proceeds from a common policy judgment – now shared by the world’s two largest economies – that outbound capital flows can themselves present national security considerations. For cross-border transactions with participants on both sides of the US–China relationship, the practical consequence is the prospect of parallel review processes, each assessing the same transaction against the national security interests of a different government, with timetable, conditionality and disclosure implications that deal teams should anticipate at term sheet stage.

Export Controls Embedded in Outbound Investment (Article 13)

Article 13 integrates the PRC export control regime directly into outbound investment activity. In carrying out outbound investment, Chinese investors must not export or use goods, technologies, services or related data whose export is prohibited by China, and may not export or use export-restricted items without authorisation. Critically, the prohibition extends beyond physical exports to the transfer of such items to other countries or regions by means of the cross-border secondment of technical personnel, organising personnel to work abroad, the cross-border provision of technical guidance or the arrangement of cross-border training.

The operative control lists include the Catalogue of Technologies Prohibited or Restricted from Export by China7 and, for goods, the catalogues issued in batches by MOFCOM, the General Administration of Customs and the Ministry of Ecology and Environment, most recently the Catalogue of Goods Prohibited for Export (Eighth Batch) effective from 1 January 2024. We are not aware of a standalone catalogue of prohibited services, however, the PRC Export Control Law (《中华人民共和国出口管制法》) subjects services relating to dual-use items, military products and nuclear items to export control. In addition, Article 14 of the 2026 Regulations confirms that export control, cross-border data flow, customs, anti-monopoly, cyber-security and related regimes apply in parallel.

For technology-intensive transactions (such as batteries and battery materials, critical minerals processing, rare earths, advanced manufacturing, artificial intelligence and biotechnology), Article 13 means that the key technical contribution of a Chinese partner may itself require export authorisation or may not be transferable at all. Joint venture technology licences, secondment arrangements, technical services agreements and training programmes should be screened against the PRC control catalogues as a discrete due diligence workstream, in the same way that transactions are screened against US, EU and UK export controls.

Investment Barriers, Countermeasures and Counter-Sanction Lists (Articles 23–25)

Articles 23 to 25 give MOFCOM and other PRC State Council departments an express statutory basis to respond to foreign measures affecting Chinese investors, responding to the proliferation of inbound investment screening, export controls and sanctions affecting Chinese capital in a number of jurisdictions. The triggers, measures and targets are summarised below.

|

Protective and countermeasure powers of the PRC authorities under the 2026 Regulations |

||

|

Trigger |

Available measures |

Targets |

|

Article 23 – Investment barrier investigations |

||

|

Chinese investors encounter trade-related investment barriers or other obstacles to investment and business operations in a host country or region. |

MOFCOM may investigate, alone or jointly with other State Council departments. Based on the findings, the authorities may adjust country-specific investment policy and prohibit or restrict the import or export of relevant goods and technologies or international trade in services. |

Host countries and regions of PRC outbound investments. |

|

Article 24 – Countermeasures against discriminatory measures |

||

|

A country, region or international organisation, in breach of international law and the basic norms of international relations, adopts discriminatory prohibitions, restrictions or other similar measures against China in investment and business operations. |

The Chinese government and its departments may take corresponding countermeasures. Pursuant to the Anti-Foreign Sanctions Law and its implementing provisions, organisations and individuals that directly or indirectly participate in formulating, deciding upon or implementing such measures may be added to China’s counter-sanction lists.8 |

Countries or regions adopting the discriminatory measures; organisations and individuals participating in their formulation, decision or implementation. |

|

Article 25 – Measures against harmful foreign conduct |

||

|

Foreign organisations or individuals: (i) endanger China’s sovereignty, security or development interests; (ii) interrupt normal transactions with Chinese enterprises, organisations or individuals contrary to normal market principles; (iii) adopt discriminatory measures against Chinese investors or their outbound investments; or (iv) unreasonably deprive or restrict the legitimate rights and interests of Chinese investors in their outbound investments. |

Prohibitions or restrictions on: China-related import and export activities; investment within China; transactions and cooperation with organisations and individuals within China; and entry into China of relevant personnel, products and means of transport. Cancellation or restriction of work, stay or residence qualifications of relevant personnel in China. |

The relevant foreign organisations or individuals, extending to organisations actually controlled by them or in whose establishment or operation they participate. |

Two features merit emphasis. First, Article 24 dovetails expressly with the Anti-Foreign Sanctions Law (《中华人民共和国反外国制裁法》) and its 2025 implementing provisions (《实施<中华人民共和国反外国制裁法>的规定》): participation in the formulation, decision or implementation of discriminatory foreign measures – including, potentially, by private organisations and individuals – can ground a counter-sanction listing. Secondly, Article 25 measures can extend to organisations actually controlled by, or established or operated with the participation of, the targeted foreign persons, creating potential exposure across corporate structures, including joint ventures and portfolio companies.

Cross-Border Data, State Secrets and Foreign Proceedings (Articles 21–22)

Article 21 encourages Chinese investors to resolve outbound investment disputes through consultation, mediation, arbitration and litigation. Article 22 then addresses a question of growing practical importance: organisations and individuals within China that participate in outbound investment-related arbitration or litigation administered outside China, or that are subject to investigation or examination by foreign judicial or law enforcement authorities, must comply with PRC laws and regulations in relation to the protection of state secrets, data security, personal information protection, technology export administration, export control and judicial assistance before providing evidence or materials abroad, and must complete the required legal procedures where approval of a competent authority is needed.

As Article 22 applies on a territorial rather than a nationality basis, the obligation extends to foreign-invested enterprises and foreign individuals operating within China, including China-incorporated subsidiaries of international groups. It sharpens an existing conflict-of-laws tension for parties simultaneously subject to foreign discovery, disclosure or regulatory production obligations and to PRC restrictions on outbound data transfer – including security assessment of outbound transfers of important data under the Cyberspace Administration of China’s Security Assessment Measures for Outbound Data Transfer (《数据出境安全评估办法》). Disclosure protocols in cross-border disputes and investigations involving China-located evidence should be designed with these regimes squarely in mind.

Duties of Chinese Investors: Approvals, Filings and Full Life-Cycle Compliance

Approval, Filing and Registration Obligations (Article 12)

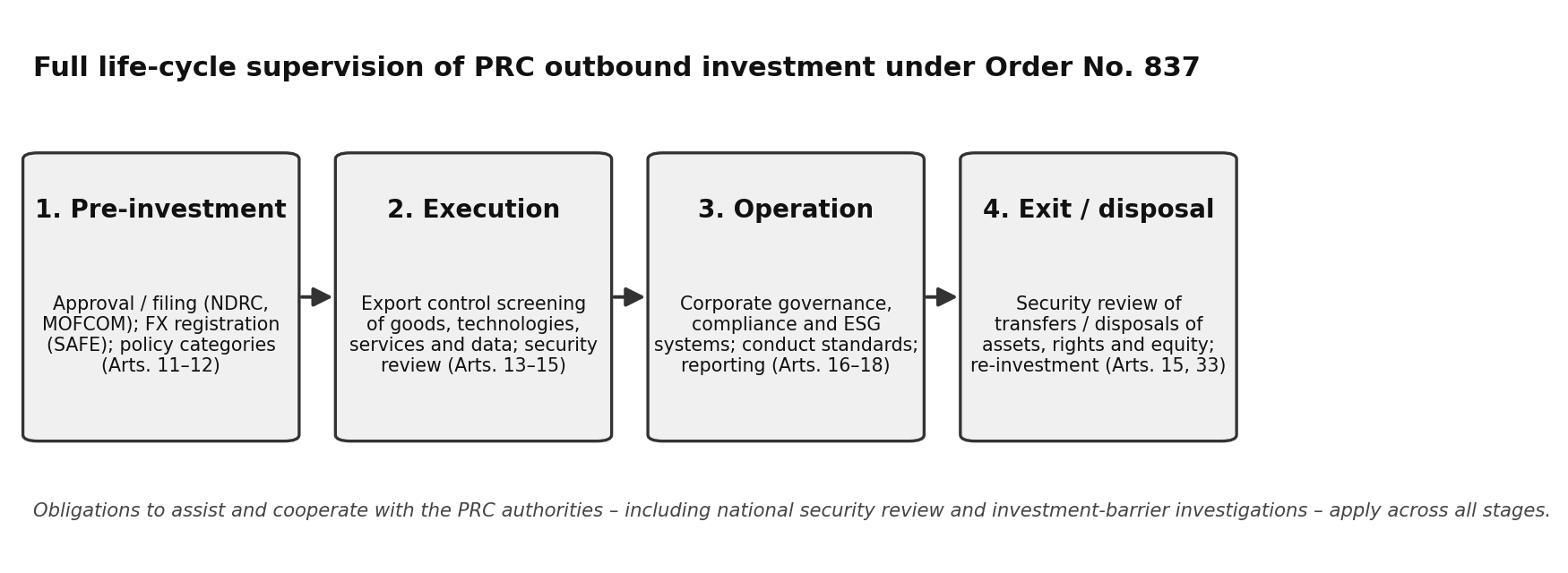

Article 12 requires Chinese investors that are obliged by law to complete approval or filing, information reporting and cross-border funds registration procedures to do so in accordance with national provisions, to submit materials truthfully and to cooperate with supervision and inspection. The operative machinery remains that of the MOFCOM Measures and the NDRC Measures: in broad terms, outbound investments constituting sensitive projects require the NDRC and MOFCOM approvals, while non-sensitive projects are subject to filings, with SAFE-supervised foreign exchange registration effected through banks.

Importantly, approval or filing obligations are not confined to the point of initial investment. Material changes, further investment (including re-investment of proceeds), and transfers or disposals during the life of a project can trigger fresh filings or approvals under the MOFCOM Measures, the NDRC Measures and the 2026 Regulations, and may attract security review as noted above. The 2026 Regulations thus confirm a full life-cycle model of supervision.

Figure 2: Full life-cycle supervision of PRC outbound investment under Order No. 837

Compliance with Host Country Laws and International Norms (Article 5)

Article 5 affirms Chinese investors’ autonomy to invest on market principles – making their own decisions and bearing their own risks – while requiring compliance with host country laws and regulations and international customary practice, respect for local customs and cultural traditions, adherence to commercial ethics, good faith and fair competition, the performance of social responsibilities and the safeguarding of China’s national image. Investors must not impair market competition, damage the environment or harm workers’ lawful rights and interests, and must not endanger China’s national security or harm national and public interests. The provision underscores the premium the PRC authorities place on responsible, locally adapted conduct as a condition of durable outbound investment.

Corporate Governance, ESG and Conduct Standards (Articles 16–17)

Article 16 requires Chinese investors and their invested enterprises abroad to improve governance structures and to establish sound systems for compliant operation, internal control, work safety and emergency response, supported by adequate personnel, funding and equipment to protect employees and assets. Article 17 prohibits conduct that disrupts the order of the outbound investment market: damaging the commercial reputation of other investors or the reputation of their goods, infringing trade secrets, dumping at unjustifiably low prices, and obtaining improper benefits through bribery or fraud. Breach of Article 17 may attract rectification orders and, where harmful consequences ensue, a ban on outbound investment of one to three years (Article 29).

Duties to Assist and Cooperate with the PRC Authorities

Across the 2026 Regulations, Chinese investors and other relevant organisations and individuals owe duties to assist and cooperate with the authorities – in national security review (Article 15), in investment barrier investigations (Article 23) and in government risk-avoidance arrangements where major emergencies such as war, civil unrest, natural disasters or epidemics occur in a host country (Article 20). The consular protection provisions of Articles 18 to 20, under which the State monitors country risk, issues alerts and assists investors and Chinese-national employees abroad, are the service-oriented counterpart of these obligations.

Enforcement and Penalties under the 2026 Regulations (Articles 27–30)

Article 27 sets the principal monetary sanctions. Failure to complete approval or filing procedures, or applying through false materials or concealment, attracts rectification orders, confiscation of unlawful gains and fines of 1‰ to 5‰ of the investment amount; refusal to rectify escalates to orders to cease the investment and dispose of shares and assets, fines of 5‰ to 10‰, and personal fines of RMB 20,000 to RMB 50,000 on responsible persons. Approvals or filings obtained by bribery, deception or other improper means are revoked, with the same fine bands and, where the investment has been made, cessation and disposal orders. From the date a penalty decision takes effect, the Chinese authorities may refuse to accept new approval or filing applications from the violator for up to three years, or ban it from outbound investment activity for one to three years. Article 30 preserves the Chinese investors’ civil, public security and criminal liability arising from breach of the 2026 Regulations.

Figure 3: Monetary penalty bands under Article 27 of the 2026 Regulations (‰ of investment amount)

The 2026 Regulations and Provisions of Anti-undue Extraterritorial Jurisdiction: A Coordinated PRC Legal Architecture for Geoeconomic Risk

The 2026 Regulations should be read alongside State Council Order No. 835, i.e., the Provisions on Anti-Undue Extraterritorial Jurisdiction by Foreign Countries (《反外国不当域外管辖条例》), issued on 7 April 2026 and effective the same day. Order No. 835 elevates China’s blocking regime from ministerial rules to State Council level. Once a foreign measure is designated as undue extraterritorial jurisdiction, organisations and individuals are generally prohibited from implementing or assisting in implementing it absent approval; foreign organisations and individuals participating in such measures may be listed on a malicious entity list (with exposure extending to affiliated entities); and Chinese parties harmed by designated measures may sue implementers in the PRC courts.

The two orders are complementary and reinforce a common theme: compliance with foreign regulatory requirements may itself become a source of legal risk in China. Order No. 835 addresses inbound legal pressure – prohibiting compliance with designated foreign measures such as certain export controls or investment restrictions – while the 2026 Regulations frame the outbound dimension, equipping the PRC State Council to respond where foreign governments or entities restrict or discriminate against Chinese investors abroad. For multinational groups, the practical consequence is a deepening tension between competing legal obligations: conduct mandated in one jurisdiction may be prohibited in another, and the implementing parties risk designation under either framework. As at the date of this Newsletter, no foreign measures have been designated and no entities listed under Order No. 835.

Implications for International Investors, Joint Venture Partners and Companies Operating in Critical Sectors

The 2026 Regulations provide the Chinese government with a comprehensive legal framework regulating the full life-cycle of Chinese outbound investment, from pre-investment approval, filing and ongoing compliance to exit. Even companies headquartered outside China may face indirect exposure through counterparties, financing sources and supply chain relationships. Sectors of pronounced strategic importance (such as critical minerals, lithium and the broader battery materials chain, rare earths, semiconductors and advanced manufacturing) sit squarely within the regulatory focus of both the PRC authorities and foreign investment screening regimes: projects in these sectors frequently involve Chinese joint venture partners, access to Chinese processing capacity or reliance on Chinese technical expertise, each of which now carries an additional layer of PRC regulatory and geopolitical risk.

International businesses with Chinese partners, investors or financing relationships should consider, in particular:

- Export control diligence (Article 13): whether proposed or existing arrangements involve goods, technologies, services or data subject to PRC export prohibitions or restrictions, with particular attention to processing technologies, secondment of technical personnel, technical services and training, and cross-border data flows.

- Counterparty and countermeasure exposure (Articles 24–25): mapping exposure to Chinese partners and financing sources in joint ventures, offtake and licensing arrangements against the countermeasure framework, including the extension of measures to controlled and affiliated entities.

- Transaction documentation: allocating regulatory change, countermeasure and forced-divestment risk through conditions precedent, termination rights, force majeure and material adverse change provisions, and specific compliance undertakings; and anticipating parallel PRC and foreign security reviews in transaction timetables and long-stop dates.

- Exit and restructuring planning (Article 15): recognising that transfers and disposals of Chinese-invested offshore assets may themselves require China’s security review (and approval), with consequences for secondary sales, refinancings and intra-group reorganisations.

- Conflict-of-laws management (Article 22 and Order No. 835): designing disclosure and discovery protocols for China-located evidence, and stress-testing group compliance policies against the possibility that foreign regulatory obligations are designated under the anti-extraterritoriality regime.

- Ongoing monitoring: establishing governance processes to track implementing rules – including the anticipated measures for outbound investment by PRC resident individuals – and any designations, listings or countermeasures activated under the new framework.

Impact of China’s 2026 Regulations

The 2026 Regulations create a more unified and authoritative legal framework for PRC outbound investment without displacing the familiar MOFCOM, the NDRC and SAFE machinery. Their significance is as much geopolitical as administrative: outbound capital is now expressly governed within China’s holistic approach to national security, export controls travel with the investment, and the PRC State Council holds a statutory toolkit of investigations and countermeasures calibrated to the external environment. For Chinese investors, the compliance perimeter now runs from first approval to final exit. For international counterparties, the message is equally clear: understanding the PRC regulatory position of a Chinese partner is no longer a matter of deal due diligence alone, but a core element of geopolitical risk management. Charltons will continue to monitor implementing rules and enforcement practice as the 2026 Regulations take effect on 1 July 2026.